Boat Financing: How to Secure a Boat Loan

Research boat financing and boat loans, and you’ll discover that financing a boat is faster and easier to attain than many people think. In most cases, securing boat financing usually isn’t very different from financing a new car.

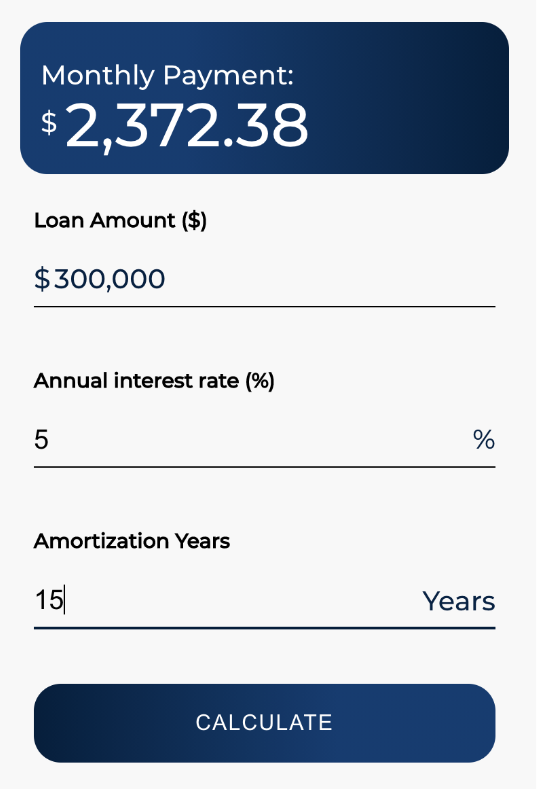

However, before you submit a boat loan application, there are a few steps you’ll need to take first. To start, you should select the type of boat you’d like to purchase. Then, estimate how much a monthly boat loan payment will cost and determine if you can afford it. We make this easy through our Boat Loan Calculator tool.

Once you’ve determined the exact model you want to buy and know the purchase price, you’ll have to choose a lender. There are many great options for boat financing providers, but doing your research first is crucial.

In this post, we’ll review boat financing basics, so you can secure funding and purchase the boat of your dreams!

Boat Financing Providers: What Are Your Options?

To finance a boat, you can go in one of three directions:

- Arrange financing through your boat dealer.

- Get a loan from your bank.

- Take out a boat loan with a lender specializing in marine financing.

Most people work through their boat dealers since dealers have experience setting up boat loans. Plus, it’s in the dealers’ interest to ensure the process is smooth, fast, and painless.

Still, other buyers will opt for financing the boat by taking out a home equity line, a second mortgage, or a personal loan from their bank. This can lead to a lower interest rate, but the downside to this option is that it can also add paperwork and make the transaction a bit more complex. However, it may be worth considering because you might also enjoy some tax benefits by structuring the deal this way.

You may also find a great deal by working with a third-party lender that offers boat loans. Members of the National Marine Lenders Association focus on financing boats. They may be able to arrange a deal with lower down payments, faster decisions, longer financing terms, or lower monthly payments.

If you’re still weighing your boat financing options, Our How to Get a Boat Loan guide has more information on securing a loan.

Typical Boat Financing Requirements

If you qualify for a car loan, you’ll probably be eligible for a boat loan. Marine lenders will take the same sorts of factors into account:

- Credit rating

- Debt to income ratio

- Job and homeownership stability

- Net worth

Again, when considering all these factors, a company specializing in boat loans generally acts the same as a company making loans on new cars.

Take your credit score, for example. If it’s 700 or above, that box is a cinch to check. If it’s in the upper 600 range, you shouldn’t have a problem getting financing, but you may get charged extra on the interest rate. Scores lower than that can become problematic, so check your credit score first.

As for the other factors, you may have to provide some information (such as a personal financial statement or employment verification).

Modern Boat Financing Options

Even if you have the cash to buy a boat on the spot, it’s crucial to consider your loan options. Financing can help you maintain liquidity, but more importantly, it might also help you purchase a more expensive boat that might otherwise seem out of reach.

Boat loans used to be more limited in duration, but now typical boat loan terms of 10 to 20 years are standard. Interest rates are very low, and the down payments required these days can range anywhere from no money down to 20 percent.

Remember, however, that if you can swing shorter terms and a higher down payment, you’ll likely get even more favorable boat loan rates. Larger boat loan amounts often get a better rate, too—so in some ways, buying the more expensive boat can actually “save” you money.

However, these aspects of boat financing are much less important than the bottom line: you get a brand-new boat—and life is about to improve. Now that’s what we call “favorable terms.”