Financing a Pontoon Boat

When purchasing a boat, most new boat owners focus on the fun stuff, such as picking out colors, upholstery options, layouts and accessories. However, an important part of the process is securing financing.

This guide will walk you through the steps from getting a boat quote to pre-approval to understanding types of loans and making payments.

Basics of Pontoon Boat Loans

How do boat loans work? If you’ve made a large purchase before, like buying a car or a house, you may be familiar with some of the basics. Financing a boat is no different.

Boat loans are typically fixed rate, fixed term, simple interest loans that are secured by the boat being purchased. Because the volume of boat sales is much lower than that of the auto industry, you may not see the same kinds of discounts, promotions or rebates you would see when buying a car and the interest rates may be higher than you are used to.

How Do Boat Loans Work?

When financing a boat, you typically will make a down payment for a portion of the purchase price and then the rest of the purchase is borrowed from a lender.

Also, if you are trading in a boat, the equity you’ve built will help reduce the total loan amount. The purchaser then pays interest over a fixed amount of time as the borrowed money is paid back.

While the loan payments of the purchase of the boat is a big portion of the overall cost of the boat, remember that there are additional costs involved in owning a boat, such as maintenance, storage, insurance and operating expenses that all need to be a part of your boating budget.

How to Get a Boat Loan

There are several institutions that offer boat loans. You can get one from a bank or credit union, or your dealer may provide financing directly. There are also marine-specific financing companies that are especially familiar with the ins and outs of boat loans.

Before applying for a boat loan, you should find out any specific requirements of the institution. If you are buying from a dealer or if the boat is new from the manufacturer, it may not be necessary, but for used boats some lenders require a marine survey, and lenders usually require insurance.

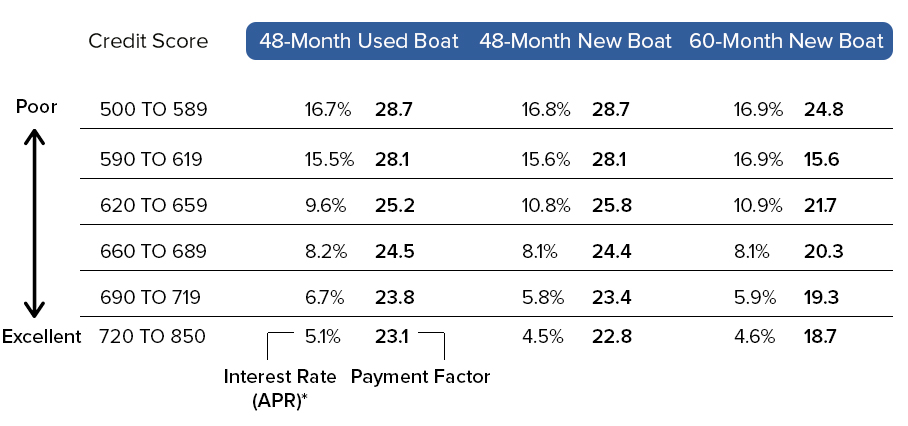

When applying for a loan, lenders will take into account the credit score, income and debt-to-income ratio and overall liquidity of the buyer.

Also, keep in mind that since the boat itself is securing the loan, your experience with boats may come into play. Factors such as the size of the down payment and the length of the loan also impact the final terms of the loan.

Boat Loan Pre-Approval

The first step in applying for a boat loan is the pre-approval. The lender will run your credit and determine if you are a candidate for the loan and how much they are willing to approve you for.

This will give you an idea of how much you will need to put down at the beginning of the loan, as well as interest rates and terms.

How Long Can You Finance a Boat

Boat financing is similar to purchasing a house. You spread the overall cost of the boat out over several years and pay interest over time.

The time you have to repay the loan is called the “term” of the loan and will impact the amount you pay on interest, as well as your monthly payments.

Boat Loan Terms

Typically, boat loans are between 10 and 20 years, depending on the down payment, credit score, income and the amount of the loan. Depending on the size of the vessel, you can negotiate for shorter loans if you wish.

You can also make additional payments to reduce the principal, but the monthly payments will remain the same during the life of the loan.

How Much are Boat Payments

Your monthly boat payments can vary based on the purchase price of the boat, down payments and the terms of the loan. You should be very sure before you sign on the dotted line that you can afford the monthly payments and that you have budgeted for maintenance, storage and operational expenses.

Boat Payments

Once you take possession of your new boat, it is vital that you stay up to date on your monthly payments. Your lender will likely have a number of ways you can pay, from auto payments, online portals to mailing in a check. Ensure that you know how to pay so you never miss a payment

Calculate Boat Payment

If you want to calculate your payment ahead of time, there are a number of online resources available to help you estimate your boat payment.

Take Over Boat Payments

One final possibility for purchasing or selling a boat is assuming a loan. If someone is selling a boat, but they still have a loan on it, you can take over their payments and ownership of their boat. If interest rates have increased, this would be a great way to get a loan with lower rates than you may be able to get at the current market.

On the other end, if you decide to sell your boat before it is paid off in full, you can offer the buyer to assume your loan. Not all lenders allow this, but it is certainly something to look in to.